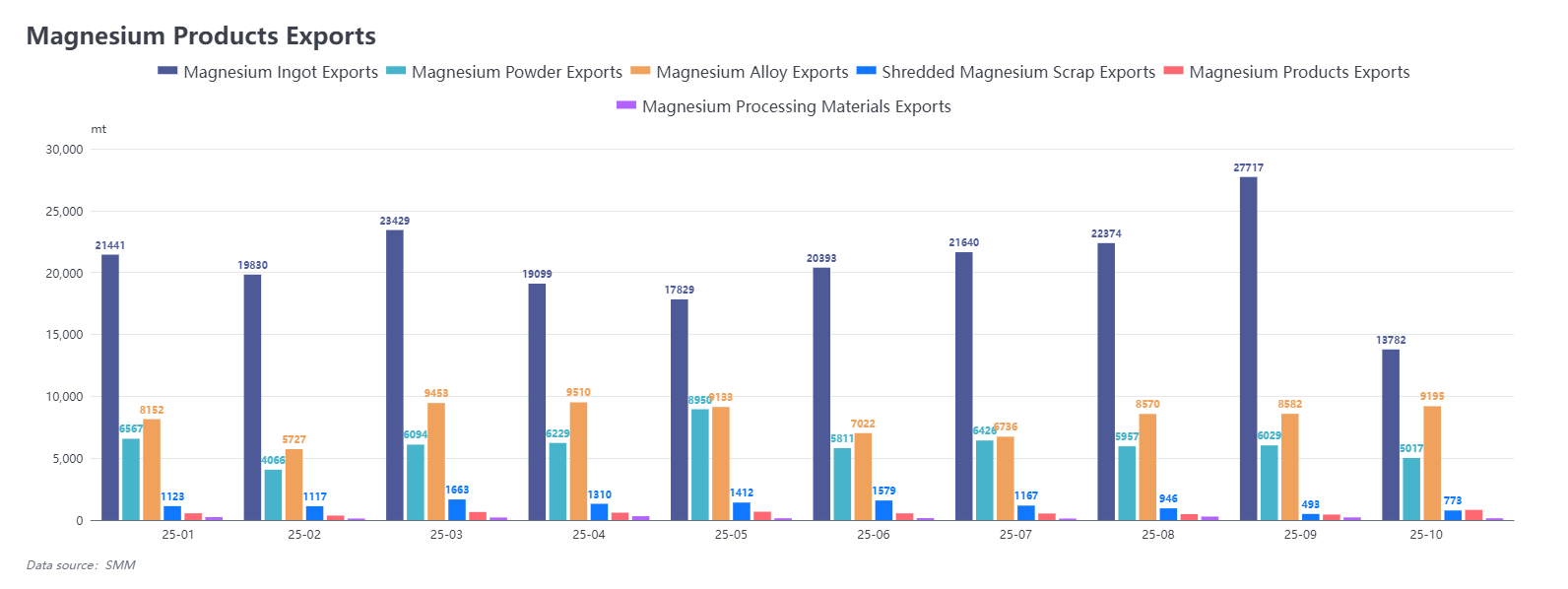

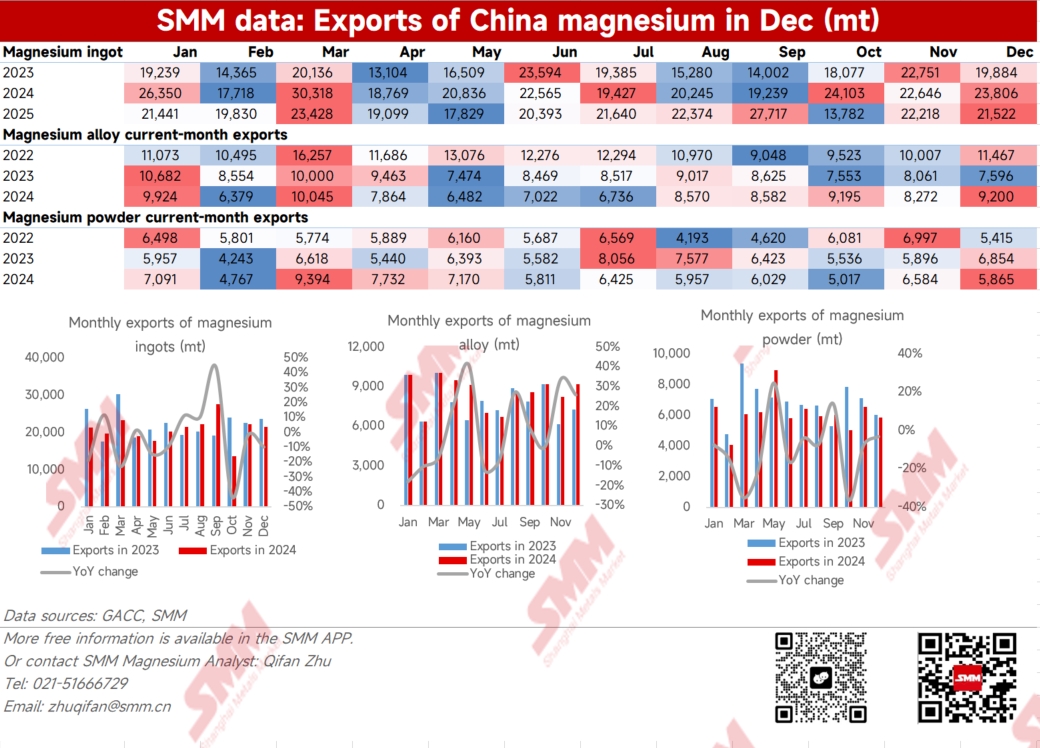

Cumulative magnesium exports in 2025 totaled 447,000 mt, down 2.7% YoY. In December 2025, China's total magnesium product exports amounted to 38,700 mt, a slight decrease of 0.5% MoM. Export volume for the month was largely flat compared with November, continuing the correction trend since the October peak.

In December 2025, domestic spot magnesium prices remained low, and overseas orders were mostly concentrated at the beginning of the month. According to trader feedback, total orders for the month were similar to or slightly lower than the same period in previous years. However, thanks to low magnesium prices, some end-users locked in long-term contracts for the next six months, providing some support for exports in 2026. Meanwhile, affected by the Christmas holiday and subsequent magnesium price corrections, overall overseas inquiries and trading activity declined noticeably from December last year to January this year.

By product:

Magnesium ingot: Cumulative exports in 2025 reached 251,300 mt, down 5.54% YoY, with December exports at 21,500 mt, down 3.13% MoM.

Throughout the year, the slight decline in exports was mainly due to structural fluctuations in Q2 and Q3. Q2 is traditionally an off-season for exports, coupled with weak end-use industrial demand in key markets such as Europe, leading to a noticeable contraction in H1 export volume. Q3 saw abnormal volatility: an initial export rush driven by policy expectations, followed by a cliff-like drop in orders after the actual policy implementation. This reflects that overseas end-users generally adopted a cautious approach during periods of policy uncertainty, preferring to control inventory and maintain purchasing as needed rather than engage in large-scale stockpiling.

Overall, magnesium ingot exports in 2025 were still dominated by actual end-use demand, with no sustained stockpiling-driven growth.

Magnesium powder: Cumulative exports in 2025 totaled 73,600 mt, down 11.07% YoY, with December exports at 5,900 mt, down 10.92% MoM.

Magnesium powder exports remained low throughout 2025, mainly due to factors such as the energy crisis, which weakened demand in Europe and led to a noticeable contraction in overseas end-use demand. This year, downstream steel market conditions were generally weak. In Europe, a major demand region, the shutdown of some steel plants further reduced overseas purchase externally demand, resulting in a significant decline in magnesium powder export volume.

Looking ahead to 2026, there are no clear signs of a market demand boost yet, and the magnesium powder export market is expected to remain in the doldrums.

Magnesium alloy: Cumulative exports in 2025 reached 99,600 mt, up 4.43% YoY, with December exports at 9,200 mt, up 11.22% MoM.

Magnesium alloy exports remained stable overall in 2025 and showed a slight increase starting in H2. This growth was mainly driven by two factors: first, production was low earlier due to production scheduling and summer maintenance in July-August, leading to a recovery rebound in exports from Q3 onward from a low base; second, the gradual acceleration in the development of overseas NEV and other application sectors, along with a rebound in technological innovation activities in 2025, boosted demand for magnesium alloys.

Looking ahead to 2026, although the growth rate of overseas magnesium alloy demand is unlikely to match the expansion pace of China's downstream market, it is still expected to maintain a mild upward trend. Exports by Destination Structure.

By country:

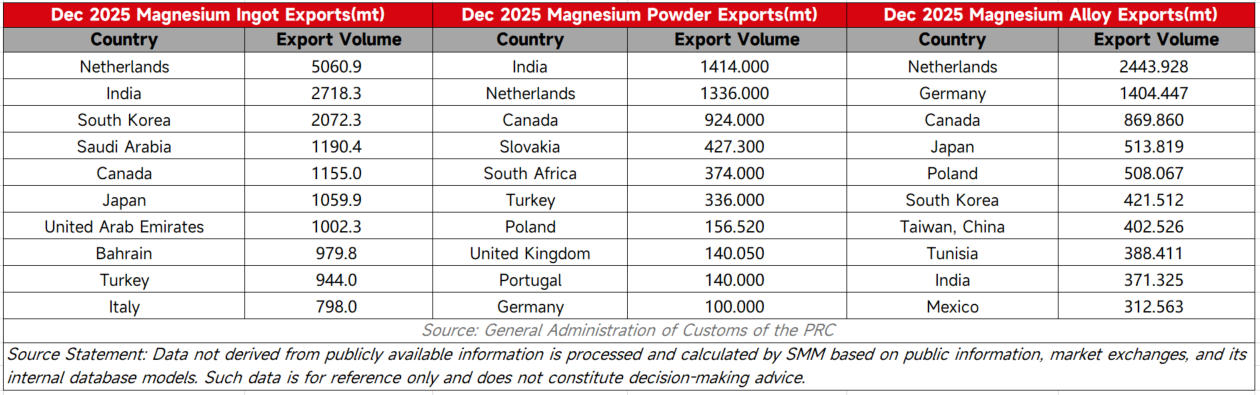

In December, magnesium ingot exports continued to be dominated by the European market, with exports to Europe reaching 5,060 mt, accounting for a relatively high proportion. Meanwhile, exports to Asian regions such as India and South Korea also showed rapid growth, becoming important supplementary markets.

In terms of magnesium powder exports, the Indian market performed prominently, with significant export growth, and together with Europe, it has formed the mainstream destinations for current magnesium powder exports, indicating a gradual increase in demand from the Asian market.

Magnesium alloy exports continued to maintain concentrated reliance on the European market, mainly flowing to traditional industrial countries such as Germany and the Netherlands, indicating that demand for high-end magnesium alloy products still highly depends on mature industry chains in Europe, such as automotive and aerospace.

2026 Outlook

Entering 2026, the magnesium product export market needs to focus on the impact of the following two policies:

First, the implementation of the joint customs and tax verification policy. On December 30, 2025, the General Administration of Customs and the State Taxation Administration jointly issued Announcement No. 256, clarifying that starting January 1, 2026, nationwide electronic data verification will be implemented for the "Certificate of Tax Refund/Not Refunded for Export Goods." This measure aims to close regulatory loopholes related to repeated declarations and improper tax refunds by enabling real-time data comparison between systems. Against this backdrop, the magnesium metal export transaction environment is becoming more standardized, with traders adopting more cautious pricing and declaration practices. Magnesium product exports in 2026 are expected to develop in a more standardized and orderly direction.

Second, the tightening of dual-use items export controls toward Japan. On January 6, 2026, the Ministry of Commerce issued the "Announcement on Strengthening Export Controls of Dual-Use Items to Japan," explicitly prohibiting the export of dual-use items to Japanese military users, military purposes, and related end-users. Magnesium, which falls under dual-use items, is included in the control scope. This means that magnesium metal exports to Japan will face stricter compliance reviews, and related trade activities are expected to become more cautious.

Looking at recent export performance, exports from November to December 2025 mainly resulted from the execution of orders signed earlier in September to October. In the short term, as overseas customers typically complete stockpiling before the Chinese New Year (February), shipments from January to early February are expected to remain at high levels, possibly even reaching periodically elevated levels. Looking ahead to the full year, magnesium ingot exports in 2026 are expected to fluctuate due to policy constraints in the Japanese market. The growth momentum for overall magnesium product exports is projected to be primarily driven by deep-processed products such as magnesium alloys.